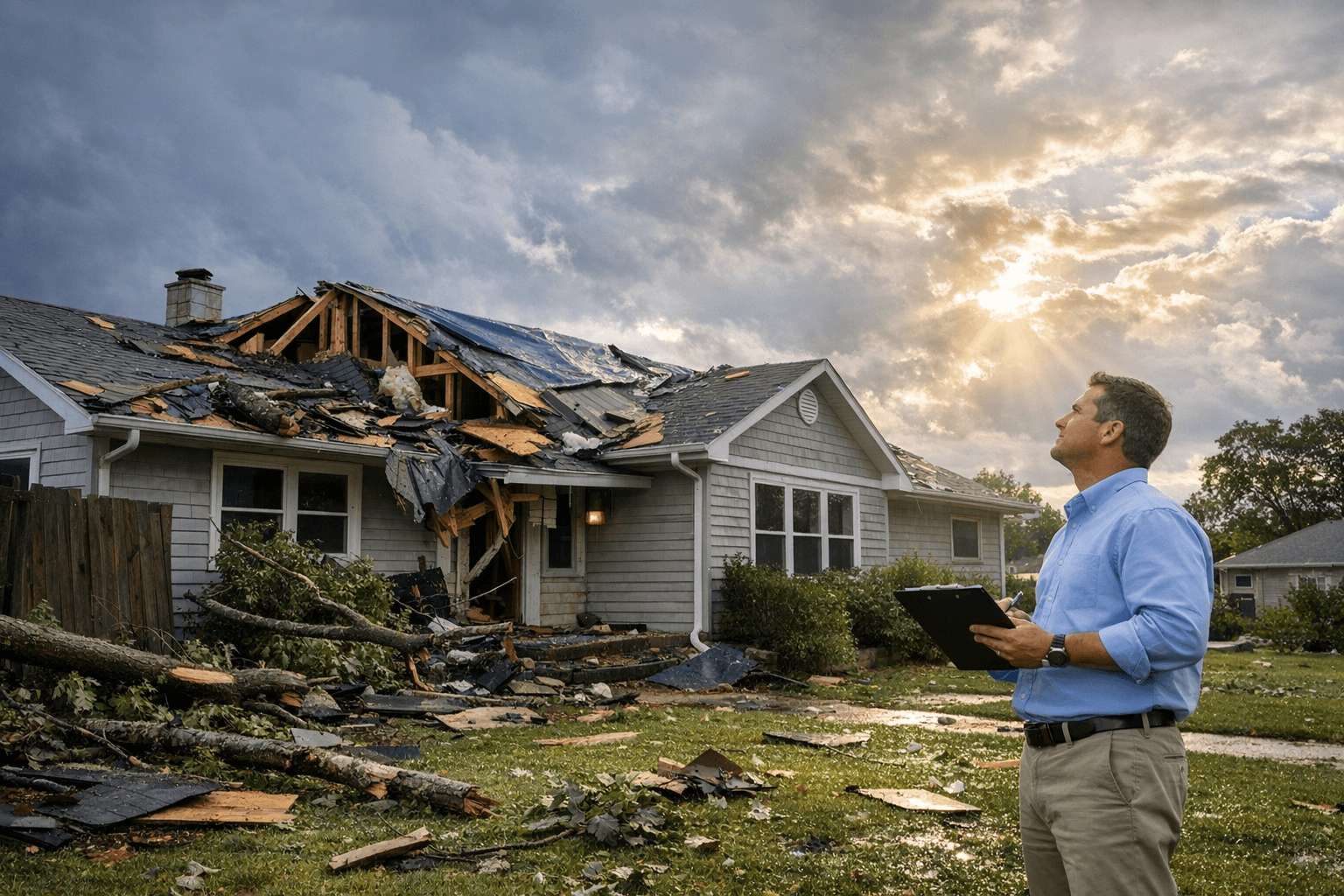

Maximize Your Roof Insurance Claim

Expert guidance to navigate claims and get the coverage you deserve

$12B

Annual Claims

65%

Underpaid

2-4x

Higher w/ Help

Your Claims Process Roadmap

Follow these steps to ensure a successful claim and maximum settlement

Safety First

Immediate

Document

24 hours

Contact Insurer

48 hours

Inspection

3-7 days

Meet Adjuster

1-2 weeks

Review Offer

2-3 weeks

Settlement

3-4 weeks

What's Typically Covered vs. Not Covered

Typically Covered

- Wind and hail damage

- Falling objects (trees, debris)

- Fire damage

- Lightning strikes

- Weight of ice and snow

- Vandalism

Typically Not Covered

- Normal wear and tear

- Poor maintenance

- Gradual deterioration

- Settling or cracking

- Mold or fungi

- Cosmetic damage only

Essential Documentation Checklist

Proper documentation is the key to maximizing your settlement

Insurance policy documents

CriticalPhotos of damage from multiple angles

CriticalPrevious inspection reports

ImportantReceipts for temporary repairs

ImportantProof of home ownership

RequiredTimeline of events

HelpfulEstimate Your Settlement

* This is an estimate only. Actual settlements vary based on policy terms.

Common Pitfalls to Avoid

Missing Deadlines

Most policies require filing within 1 year of damage

Accepting First Offer

Initial settlements are often 10-20% below actual costs

Using Wrong Contractors

Always verify insurance approval before starting work

When to Hire a Public Adjuster

Consider Professional Help When:

- Claim exceeds $10,000

- Insurance company disputes coverage

- Multiple types of damage involved

- You lack time to manage the claim

- Initial offer seems too low

Average Results:

* Based on average settlements. Individual results vary.

Most homeowners leave thousands on the table during roof insurance claims. This guide shows you exactly how to document damage, work with adjusters, and maximize your settlement.

Whether you're dealing with storm damage, hail, or other covered perils, understanding the insurance process is crucial. Follow this guide to ensure you get fair compensation for your roof repairs or replacement.

Detailed Step-by-Step Claims Process

Ensure Safety & Prevent Further Damage

Your safety comes first. Once safe, take reasonable steps to prevent additional damage:

- Cover holes with tarps (keep receipts for reimbursement)

- Document all temporary repairs with photos

- Don't make permanent repairs before adjuster visit

- Move valuables away from leaks

Document Everything Thoroughly

Proper documentation is crucial for a successful claim:

Photo Checklist:

- Wide shots of entire roof from multiple angles

- Close-ups of all damaged areas

- Interior damage (ceilings, walls, attic)

- Damaged personal property

- Date/time stamps on all photos

- Reference objects for scale (ruler, coin)

Contact Your Insurance Company

Call your insurer as soon as possible to start the claim:

- Have your policy number ready

- Report date and cause of damage

- Get claim number and adjuster contact

- Ask about coverage limits and deductibles

- Request email confirmation of claim filing

Get Professional Inspection

Don't rely solely on the insurance adjuster's assessment:

- Hire your own roofing contractor for inspection

- Get detailed written damage assessment

- Request itemized repair estimate

- Have contractor present during adjuster visit

- Document any disagreements

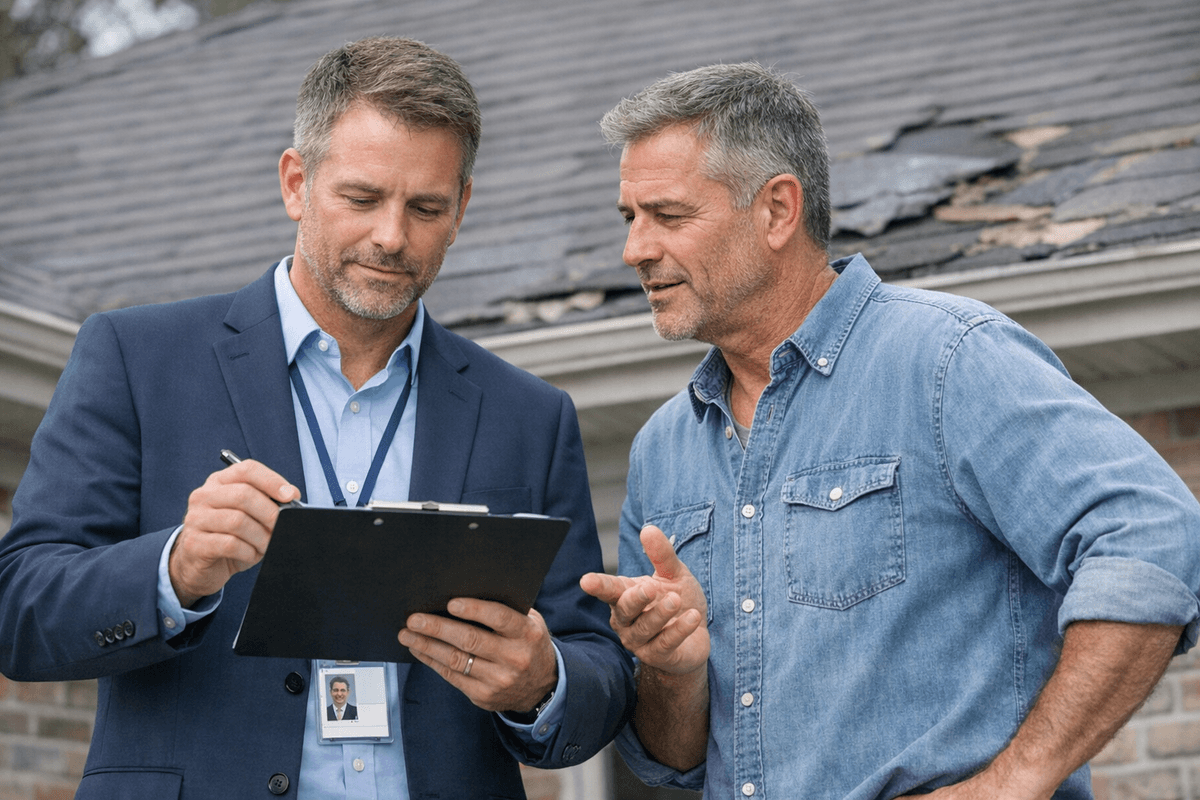

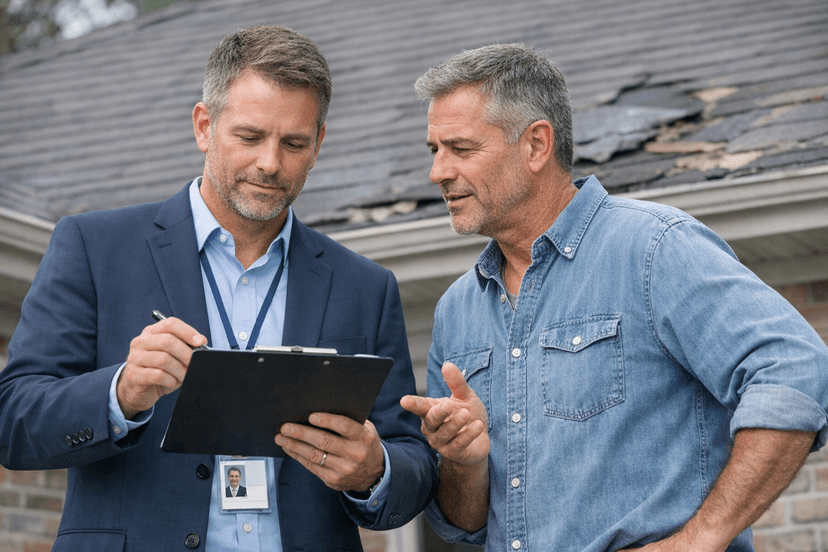

Meet with Insurance Adjuster

Be prepared and present during the inspection:

Adjuster Meeting Tips:

- Point out all damage areas

- Provide your documentation

- Take notes and photos of inspection

- Get adjuster's report in writing

- Don't sign anything immediately

- Ask questions about their findings

Review Settlement Offer

Carefully review the insurance company's offer:

- Compare to contractor estimates

- Check for missing damage items

- Verify pricing matches local rates

- Understand depreciation calculations

- Know your deductible amount

Negotiate if Necessary

Don't accept a low offer without discussion:

- Present contractor estimates as evidence

- Request re-inspection if damage missed

- Invoke appraisal clause if available

- Consider hiring public adjuster (10-15% fee)

- Document all communications

Common Mistakes to Avoid

❌ Waiting Too Long to File

Most policies require prompt reporting. Delays can lead to denial.

❌ Throwing Away Damaged Materials

Keep samples for adjuster inspection unless they pose safety risk.

❌ Accepting First Offer Immediately

Initial offers are often 20-50% below actual costs.

❌ Not Getting Multiple Estimates

One estimate leaves you without negotiation leverage.

❌ Signing Over Benefits to Contractors

Keep control of your claim and payment process.

Tips for Maximizing Your Settlement

Documentation Power

- • Keep maintenance records showing roof care

- • Save receipts for all temporary repairs

- • Create timeline of damage discovery

- • Video walkthrough with narration

- • Weather reports from damage date

- • Before photos if available

Professional Support

- • Experienced roofing contractor advocate

- • Public adjuster for large claims

- • Attorney for bad faith denials

- • Engineer reports for structural issues

- • Drone inspection documentation

- • Code upgrade requirements

Understanding Your Settlement

Key Terms Explained

- Replacement Cost Value (RCV)

- Full cost to replace your roof with similar materials at today's prices

- Actual Cash Value (ACV)

- RCV minus depreciation based on roof age and condition

- Depreciation

- Reduction in value due to age (recoverable in most policies)

- Deductible

- Your out-of-pocket amount before insurance pays

- Supplemental Claim

- Additional payment request for missed damage or increased costs

Typical Payment Structure

- First Check: ACV minus deductible (immediate)

- Second Check: Recoverable depreciation (after completion)

- Supplements: Additional damage found during work

Insurance Claim Red Flags

⚠️ Watch Out For:

Storm Chasers: Out-of-state contractors who appear after storms, often with high-pressure tactics and assignment of benefits schemes.

Lowball Estimates: Adjusters using outdated pricing or missing obvious damage to minimize payouts.

Policy Exclusions: Suddenly discovered limitations that weren't clearly explained when you bought coverage.

Delay Tactics: Repeated requests for documentation you've already provided or unreasonable investigation timelines.

When to Hire Professional Help

Public Adjuster

Consider when:

- Claim exceeds $10,000

- Extensive hidden damage

- Initial offer seems low

- Complex claim issues

Attorney

Necessary when:

- Claim wrongfully denied

- Bad faith suspected

- Policy interpretation disputes

- Significant underpayment

Engineer

Helpful when:

- Structural damage present

- Cause of damage disputed

- Code compliance issues

- Foundation affected

Your Insurance Claim Checklist

Print and Use This Checklist:

Need Help with Your Insurance Claim?

Our network of certified contractors works directly with insurance companies to maximize your settlement.